Hello world!

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text…

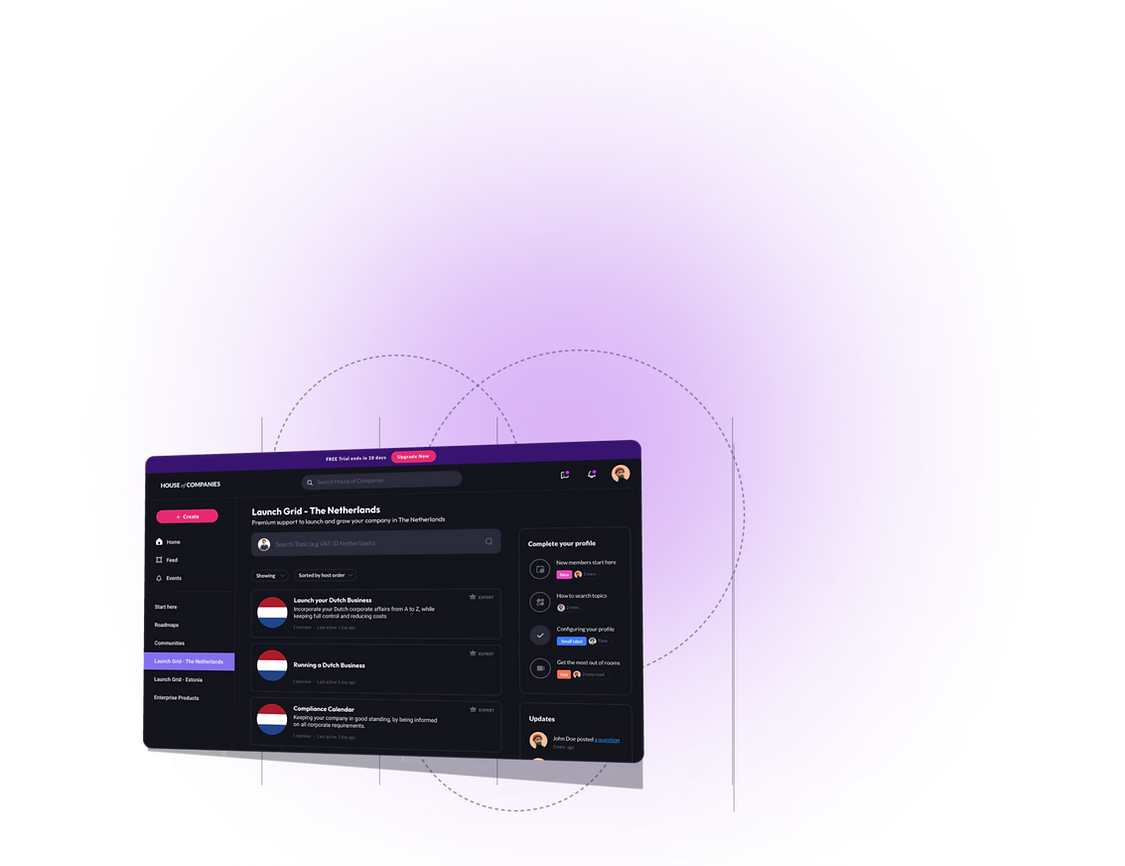

Explore House of Companies' innovative platform tailored for Croatian entities to manage their financial data collection and compilation. This platform seamlessly integrates data, documents, and team communication.

Croatian entities can ensure their financial data is comprehensive and compliant, establishing a solid foundation for the accurate preparation of financial statements. Faster and more efficient than ever!

Delivering and processing invoices, bank statements, and agreements (like your lease) is becoming simpler every day. House of Companies streamlines the submission of your data using a single source for all documents, data, and reports. Track our progress and your profits in real-time!

Despite the ever-expanding nature of tax and accounting playbooks and support, your situation might require the assistance of a Croatian chartered accountant. If you need help filing your tax return, House of Companies is here to assist.

You can either send us your existing ledgers and VAT Analysis or instruct us to draw up new ones from scratch.

In the process of establishing and scaling a Croatian LLC, learning how to prepare Financial Statements in Croatia is crucial. It goes beyond legal compliance and is essential for transparency, financial health tracking, and decision-making. Financial statements, including the balance sheet, profit and loss account, and auditor's report, showcase fiscal responsibility and operational efficiency to shareholders, potential investors, and regulatory bodies.

This guide provides a structured pathway to prepare financial statements according to Croatian regulations and standards. It covers gathering and compiling financial data, complying with Croatian Generally Accepted Accounting Principles (GAAP), understanding legal entities and filing requirements, and the role of chartered accountants in Croatia. It also discusses the submission process, filing financial statements at the Croatian Chamber of Commerce, and preparatory work for Corporate Tax analysis and submission. The article includes insights into the simplified procedure for micro and small entities, filing deadlines, and the eHerkenning tool for digital submissions. It serves as a comprehensive roadmap for Croatian LLCs navigating the legal landscape of financial reporting.

Croatian LLCs are required to prepare a comprehensive set of financial documents, including the balance sheet, profit and loss account, and notes explaining these documents. For small entities, these statements need not be audited, but they must still provide a clear picture of the company's financial status.

The collection of financial data can be significantly enhanced by using advanced tools and software that automate and streamline the process. For instance, platforms that offer real-time ledger generation and tracking help maintain up-to-date financial information, promoting transparency and reducing the risk of misstatements. Additionally, tools that support the scanning and organized storage of documents facilitate the efficient extraction and processing of data, ensuring that all financial information is accurately captured and readily available for reporting.

In Croatia, the preparation of financial statements for a Croatian LLC must adhere to specific standards to ensure transparency and compliance. These standards dictate the inclusion of the balance sheet, income statement, and, depending on the size of the company, the cash flow statement.

The balance sheet is a fundamental element of financial statements, providing a snapshot of the company's financial position at a given time. It includes assets, liabilities, and shareholders' equity, formatted according to the Decree on financial statements formats, which specifies the layout for companies, excluding micro companies. The balance sheet must balance the equation where total assets equal the sum of liabilities and shareholders' equity.

The income statement, or profit and loss account, details the company's financial performance over the financial year. It includes both realized and unrealized profits and losses, reflecting income from investments and operational activities. This statement also features distinct categories for dividends and taxes paid, which are specific to the Croatian context. It provides insights into the company's revenue streams and the efficiency of its operations.

For medium-sized and large companies, a cash flow statement is required and is considered a primary financial statement alongside the balance sheet and income statement. This statement categorizes cash flows into operating and investing activities, offering a detailed view of the company's liquidity and financial flexibility.

Leveraging modern technology, the House of Companies portal facilitates the real-time generation and tracking of financial statements. This platform integrates seamlessly with existing financial systems, allowing Croatian LLCs to maintain accurate and up-to-date records. The portal supports the automation of the balance sheet and profit and loss account creation, ensuring compliance with Croatian GAAP and reducing the risk of misstatements. This tool is invaluable for Croatian LLCs looking to streamline their financial reporting processes and ensure accuracy in their financial disclosures.

By adhering to these standards and utilizing advanced tools like the House of Companies portal, Croatian LLCs can effectively prepare their financial statements, ensuring they meet the regulatory requirements and provide valuable insights into their financial health.

Ensuring compliance with Croatian Generally Accepted Accounting Principles (GAAP) is critical for Croatian LLCs to maintain transparency and legal integrity in financial reporting. Croatian GAAP, influenced by EU directives, sets a framework that mandates financial information to be understandable, relevant, reliable, and comparable.

Under Croatian law, the financial statements must accurately reflect the company's financial position, presenting the equity at the balance sheet date and the profit for the year fairly and consistently. This includes a comprehensive balance sheet, profit and loss account, and explanatory notes. Specific valuation and disclosure requirements must be adhered to, ensuring that all financial reports provide insight into the company’s solvability and liquidity.

Failure to comply with Croatian GAAP can lead to significant consequences for Croatian LLCs. Non-compliance may result in the rejection of the financial statements by auditors, legal penalties, or financial discrepancies reported to the authorities. This can affect the company’s reputation and its ability to secure future financing or partnerships.

Directors hold a significant responsibility under Croatian corporate law. They are required to ensure that all financial reporting complies with Croatian GAAP. If directors fail in their duty of care, they may be held personally liable for any resultant damages to the company.

This includes scenarios where poor financial governance leads to bankruptcy or legal issues. Directors must act with due care and attention to avoid personal liability.

By adhering strictly to Croatian GAAP, directors not only safeguard themselves from potential liabilities but also uphold the financial integrity and trustworthiness of their Croatian LLC.

In the intricate financial landscape of Croatia, the role of a chartered accountant, particularly in external auditing, becomes indispensable for Croatian LLCs. These professionals, governed by stringent regulations and possessing specialized training, ensure that financial statements not only adhere to Croatian GAAP but also present a true and fair view of the company’s financial health.

External auditing, conducted by certified accountants, is crucial for verifying the accuracy of financial statements against the International Financial Reporting Standards. Such audits provide an independent assessment, ensuring that the financial representations made by a company are both accurate and compliant with the required standards. This process is not only beneficial but often necessary to maintain transparency, enhance credibility, and uphold the integrity of financial reporting.

For Croatian LLCs, the input of a chartered accountant can be particularly valuable in scenarios where unbiased, expert verification of financial records is required. This includes situations where internal audits may not suffice due to potential biases or the internal auditor’s proximity to daily management, which might delay or color the reporting of crucial financial information. External auditors bring a level of detachment and expertise that significantly mitigates these risks.

Moreover, engaging with external auditors can lead to the discovery of discrepancies or potential areas of fraud, providing management with critical insights into possible risks and the overall financial health of the company. The feedback and strategic advice offered by these auditors can drive improvements in financial practices and controls, directly influencing the operational efficiency and profitability of the business.

In addition to ensuring compliance and enhancing transparency, external auditing also plays a pivotal role in reinforcing the confidence among shareholders and investors. It assures them of the company’s commitment to financial accuracy and reliability, which is particularly crucial for attracting investment and supporting business growth.

The regulatory framework in Croatia mandates that chartered accountants undergo rigorous postgraduate training, focusing on areas like financial auditing and external reporting. This training ensures that they are not only well-versed in the theoretical aspects of their field but are also adept at applying this knowledge practically, thereby supporting businesses effectively through their expertise in auditing and financial scrutiny.

In conclusion, the involvement of a chartered accountant in the external auditing of Croatian LLCs is not just a regulatory formality but a strategic business imperative. It supports robust financial governance, fosters trust among stakeholders, and ensures that the business can navigate the complexities of financial reporting with confidence and accuracy.

To ensure regulatory compliance and transparency, Croatian LLCs must file their annual financial statements with the Croatian Chamber of Commerce in a timely manner. This process is crucial for maintaining the legal and financial integrity of the business.

The board of directors is responsible for preparing the annual accounts within five months after the financial year ends. These accounts are then presented to the shareholders, who have two months to adopt them. Following adoption, the financial statements must be filed with the Croatian Chamber of Commerce within eight days.

If the financial year aligns with the calendar year, the latest filing date without extension is 8 August. For businesses operating under a d.o.o. structure, the final filing date extends to 8 November if the book year equals the calendar year.

In exceptional circumstances, shareholders may grant a five-month extension to the board for preparing the financial statements. However, if the accounts are not adopted within the allotted time, the unadopted accounts must still be filed.

Specifically, a d.o.o. must file these unadopted accounts within seven months from the end of the financial year; with a granted extension, this deadline can extend up to 12 months.

It is also possible to request an exemption from filing financial statements due to 'serious reasons,' such as technical impossibilities for the directors to prepare, present, or adopt the statements. These exemptions must be filed with the Croatian Chamber of Commerce Backoffice Declarations.

To ensure compliance and accuracy in financial reporting, Croatian LLCs must diligently prepare and submit their corporate tax returns. The process involves a series of critical steps, each designed to reflect the company's financial activities accurately over the fiscal year.

Corporate taxpayers in Croatia are obligated to file their tax returns annually, with a general deadline set at five months following the end of the financial year. However, extensions can be requested if more time is needed to prepare accurate and comprehensive filings.

The calculation of CIT is based on the company's taxable profits, which may include adjustments such as loss carryforwards and carrybacks. The Croatian tax authorities often issue a provisional assessment, which is adjusted after the final tax return is submitted. The final CIT assessment must be issued within three years of the financial year's conclusion, extended by any period granted for filing the return.

Interest on CIT due is calculated from six months after the end of the financial year until the assessment is issued, with the current interest rate set at 10% for 2024. If the CIT is paid late, a lower interest rate of 4% applies, calculated from six weeks after the issuance of the assessment.

Croatian LLCs may be audited by tax inspectors as part of the national tax authorities' vertical monitoring tasks. This scrutiny ensures that all financial activities and tax filings are transparent and adhere to Croatian regulations. Enhanced cooperation between taxpayers and tax authorities has been noted, potentially easing the compliance burden.

Corporate tax returns must be filed digitally. Companies have the option to manage this process in-house using approved software or outsource it to a tax service provider. For those needing more time, filing extensions can be applied for through the Croatian Tax Administration's website or by submitting a form.

For foreign taxpayers earning income in Croatia, it's crucial to understand the implications of international tax treaties, which prevent double taxation on the same income. This ensures that companies are not unfairly taxed by multiple jurisdictions.

By following these guidelines and utilizing available resources, Croatian LLCs can effectively manage their corporate tax obligations, ensuring compliance and contributing to their overall financial health.

How can one access the financial statements of companies in Croatia?

You can obtain the financial statements of Croatian companies by ordering them online through the Croatian Chamber of Commerce, for which a fee is charged.

What type of accounting system is prevalent in Croatia?

Croatia employs a double-entry bookkeeping system for accounting. This method mandates that every financial transaction is recorded with both a debit and a credit entry.

Are the financial statements of companies publicly available in Croatia?

In Croatia, companies are required to prepare annual financial statements and have them approved by their shareholders. These financial statements are generally made public by being filed with the Croatian Chamber of Commerce.

Which accounting standards do Croatian companies adhere to?

Croatian companies that are listed on an EU/EEA securities market have been following the International Financial Reporting Standards (IFRS) since 2005. The European Commission also releases documents summarizing how the IAS Regulation options are utilized by EU Member States.

[1] - https://www.houseofcompanies.io/

[2] - https://www2.deloitte.com/content/dam/Deloitte/nl/Documents/audit/deloitte-nl-audit-annual-accounts-in-the-netherlands-2019.pdf

[3] - https://theaccountingjournal.com/netherlands/financial-reporting-in-the-netherlands/

[4] - https://online.hbs.edu/blog/post/how-to-prepare-an-income-statement

[5] - https://www.youtube.com/watch?v=aRL1MDYFMZ4

[6] - https://www.tax-consultants-international.com/publications/accounting-and-audit-requirements-in-the-netherlands

[7] - https://www.bnnlegal.nl/en/services/insolvency-law-and-bankruptcy/directors-liability-in-the-netherlands/

[8] - https://www.linkedin.com/pulse/7-reasons-conduct-external-audit-uae-atif-iftikhar

[9] - https://www.nba.nl/opleiding/foreign-auditors/ra-qualifications/the-dutch-educational-system-for-register-accountants/

[10] - https://www.kvk.nl/en/filing/when-do-i-have-to-file-my-annual-accounts/

[11] - https://www.kvk.nl/en/filing/am-i-required-to-file-annual-reports-and-accounts/

[12] - https://taxsummaries.pwc.com/netherlands/corporate/tax-administration

[13] - https://business.gov.nl/regulation/corporate-income-tax/

[14] - https://business.gov.nl/finance-and-taxes/business-taxes/filing-tax-returns/filing-your-corporate-tax-return-vpb-in-the-netherlands/

Try out the Portal of House of Companies to deal with your Annual Financial Statement requirements in Croatia, at a fixed fee, with minimal involvement of an accountant. Simplifying this process through advanced technology not only bolsters accuracy but also frees valuable resources, allowing businesses to focus on core activities that drive growth and profitability.

"I expected to take about 2 quarters to generate turnover in Germany. Luckily I didn’t have to spend any money on an accountant in the meantime."

Global Talent Recruiter

Global Talent Recruiter"My Indian accountant drafts my VAT Reports, and submits the return using Entity Management!"

Spice & Herbs Export

Spice & Herbs Export"The practical know-how in Entity Management made me comfortable to get more involved in my own tax filing! And it worked!"

IT firm

IT firmFeel welcome, and try out our solutions and community,

to bring your business a step closer

to international expansion.

Got questions?

Lets talk about your options

Stay updated with the latest news and exclusive offers. Subscribe to our newsletter for regular insights delivered to your inbox!